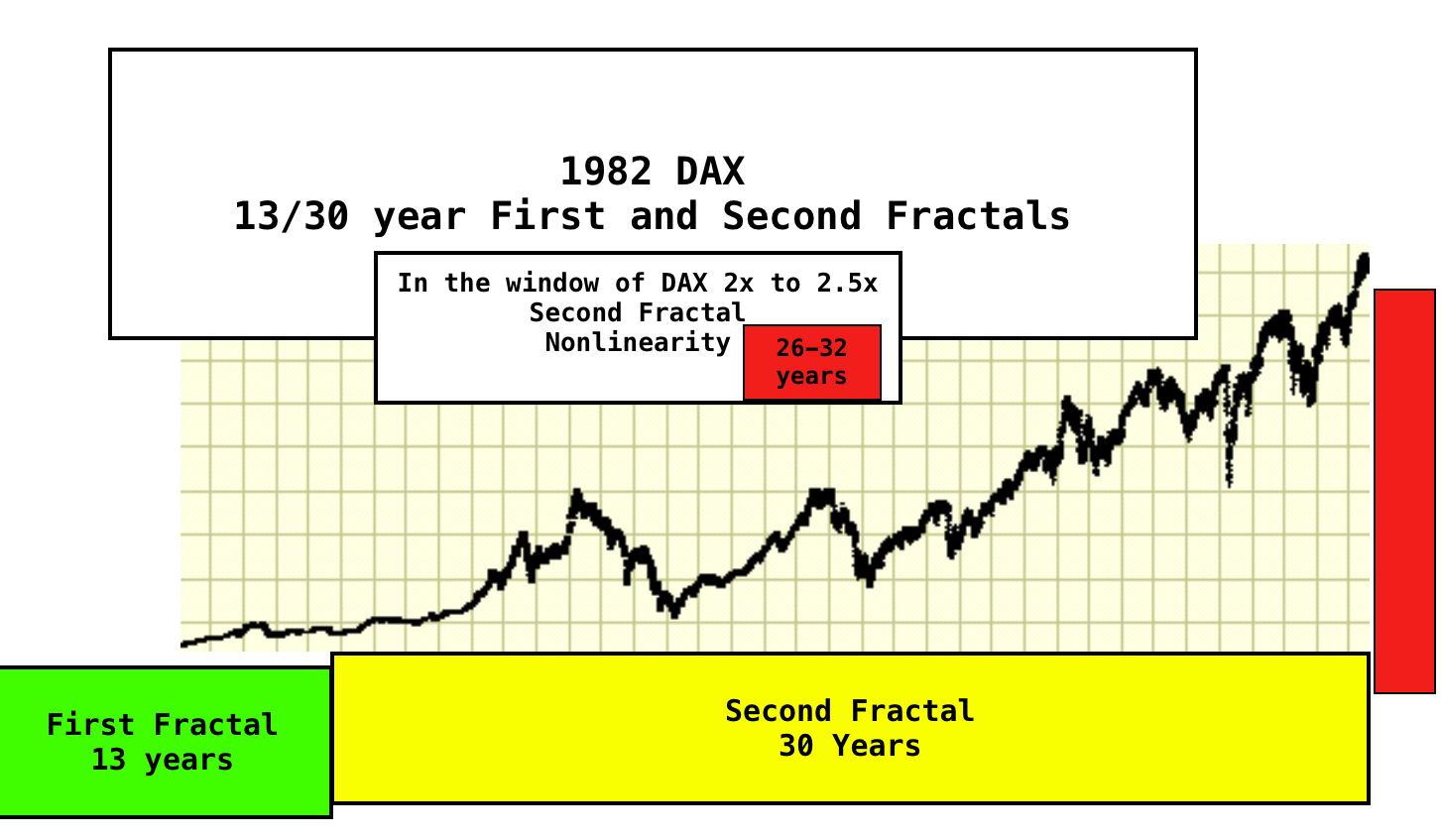

The 1982 -2024 German DAX 13-14/30-31 year First and Second Fractals

Within the 4-phase 267 year 1807 to 2074 US hegemonic x/2.5x/2.5x/1.5x :: 36/90/90/54 year fractal series, rests an interpolated 1982 German DAX 13-14/30-31 year series. The 30 year second fractal nonlinearity could as an incipient feature have an initial shocking flash crash (with a sharp rebound beyond the November 2024 election.

The self-assembly fractal mathematical architecture of the 23 October 2023 to 5 July 2024 x/2x :: 13(-)/25-26 week :: 60/120 day fractal series is observable. Rather than 28 October 2023, the Incipient day for the 13-/25-26 week first and second fractal series is 23 October 2023 consistent with the fractal maxim that fractal valuation growth begins in terminal fractal decay. Objectively, a 13(-)/25 week first and second fractal series can be identified from 23 October 2023 to 5 July 2024. The first 13 week fractal occurs as a 3/7/5 week fractal series(x/2-2.5x/1.6x) and the second fractal, a 5/10/12 of 12-13 week fractal series x/2x/2.4x-2.5x. Next trading week, the 23 Oct 2023 x/2x series with a base (x) of slightly less than 13 weeks will be in the window (2x to 2.5x)of 26-32 week second fractal nonlinearity.

As of 5 July 2024, a 23 October 2023 60/120 day :: x/2x first and second fractal series is observable. The terminal fractal window begins next week between day 121 and day 150.

The Dax is at/near its March 2020 third fractal apogee with a three phase fractal growth series of 8/24/23 months as of 5 July 2023. (see below.)

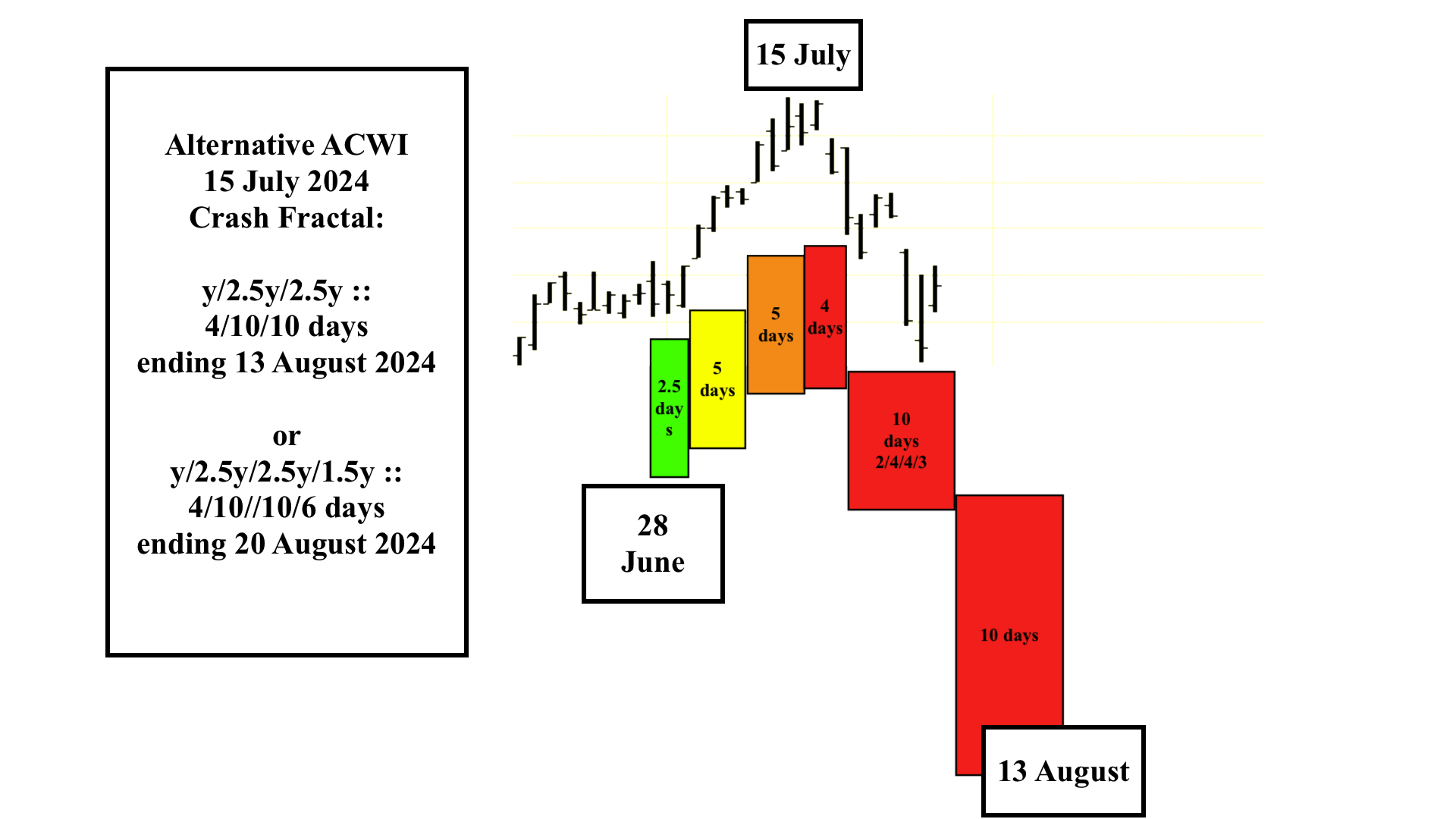

The extended second fractal of 24 months or 4/9/8/6 months :: x/2-2.5x/2x/1.5x is beyond the expected 2.5x or 20 months of the 8 March 2020 base fractal because of the extraordinary QE in 2020-2021 with the Fed adding 10-11 trillion dollars to their balance sheet or a historical 30 % increase in the GDP/national debt ratio in just two years. The last 5/10/10 month third fractal takes the DAX to its July 2024 lower high with a potential high next week completing a 4/10/6-10 day:: x/2.5x/1.5-2.5x 3-phase growth fractal series.(see the final green/yellow/orange 4/10/4 of 4-10 day growth series above).

From the 2005 main page of the Economic Fractalist regarding the nonlinearity of second fractals: The ideal growth fractal time sequence is X, 2.5X, 2X

(to 2.5x) and 1.5-1.6X. The first two cycles include a saturation transitional point and decay process in the terminal portion of the cycles.

A sudden nonlinear drop in the last 0.5x time period of the 2.5X is the hallmark of a second cycle and characterizes this most recognizable cycle. After the nonlinear gap drop, the third cycle begins. This means that the second cycle can last anywhere in length from 2x to 2.5x. The third cycle 2X is primarily a growth cycle with a lower saturation point and decay process followed by a higher saturation point. The last 1.5-1.6X cycle is primarily a decay cycle interrupted with a mid area growth period. Near ideal fractal cycles can be seen in the trading valuations of many commodities and individual stocks. Most of the cycles are caricatures of the ideal and conform to Gompertz mathematical type saturation and decay curves.